EXECUTIVE SUMMARY

India, the second largest populated country of the world, is predominantly rural in nature. Despite 72% population living in rural areas, the socio-economic conditions of most of the villages have been pathetic. Absence of basic telecom infrastructure and suitable policy initiatives has hampered addressing of issues like literacy, primary health care, rural banking etc through Information and Communication Technologies (ICT). The ICT sector is one of the prime support services needed for rapid growth and modernization of various sectors of the economy and is also vital for social development of the country. The same was well understood by policy makers in India and was iterated in the Indian Telecom policies of 1994 and 1999, which envisaged a conducive and enabling environment to facilitate the country’s vision of becoming an IT super power. In 2005, if we look back, we will find that many of the targets set by these policies have been achieved in totality but, a deep insight into the facts and figures will reflect a glaring disparity between rollout of ICT services in urban and rural India. The writing on the wall is clear. The implementation of new telecom policy has left India divided – digitally. Therefore, it is vital that an enabling environment through policy and regulatory measures is created for the transformation of the existing digital divide into digital opportunity, which also has been a key driver behind the World Summit on the Information Society (WSIS).

In such a scenario it becomes necessary for India to look towards some of the developing countries which are similarly placed as India and draw lessons for developing the ICT facilities in rural and remote areas at lowest possible costs. The growth of ICT in urban India has been mainly demand driven. But, increasing the penetration of ICT in rural India will require greater effort on supply side i.e. policy initiative from state. Scanning the world horizon, we find that despite economic slowdown, Egypt rose strongly in ICT diffusion ranking from 154th position to 112th position worldwide mainly because of policy leadership in areas of building public-private collaboration in ICT deployment.

This policy paper analyzes the reasons for skin deep telecommunication revolution in India and groups the efforts made in India to bridge the digital divide. It explores the effectiveness of Egypt’s policy initiatives for ICT diffusion like “PC for community” and “IT Clubs” and recommends how such initiatives can be customized and replicated for bridging the digital divide in India.

“PC for Community” policy offers affordable, Internet-enabled computers payable through installments, with telephone line as a guarantee and no requirement of deposits. The computer hardware is provided by various manufactures, finances are provided by major banks and the telephone line provision and installment collection is done by Telecom Egypt (TE). The Ministry of Communications and Information Technology (MCIT)’s role is to certify and monitor the performance of the companies from the private sector that have joined the program. The policy targets to create 14 million new user base for Internet and provides for building the foundation of Egypt’s Information society initiative.

The “IT Clubs” model is another Public Private Partnership to bring affordable Internet access throughout the country to those who cannot afford to own a PC.. The model was developed to offer a communal solution to one of the biggest problem encountered by emerging economy to develop Information society i.e. the problem of affordability, accessibility and awareness. MCIT is forming partnerships with Egyptian and international entrepreneurs to accelerate the rate of expansion of IT clubs, which currently number more than 1000. IT clubs are now extending their services by providing library in each club, providing e-government services, providing e-learning services etc.

If India has to consolidate its positions as a leading hub of communication systems & IT enabled services and has to establish itself as a leader in new disciplines such as bioinformatics and biotechnology, it has to quickly adopt the successful policy initiative models from the developing and developed world. Only then, ongoing IT process in India can transform into a “True Revolution”.

INTRODUCTION

India, the second largest populated country of the world, is predominantly rural in nature. Of the 1.027 billion Indians, 741 million live in 638635 villages scattered all across the country. The population density in rural India is around 300 per sq km , which is quiet high in comparison with most of the other countries. Despite this the socio-economic conditions of most of the villages has been pathetic. The literacy rate in rural parts of India is 49.4% as compared to 70% in urban India. The lopsided development is further suggested by the fact that three out of every four villages do not even have the primary health centre. Over 70 % of the rural population contributes to only 24% of GDP. Poor infrastructure and lack of banking facility have further hampered the economic growth in rural areas. Information and Communication Technologies (ICT) have been seen as a major tool that can address many of these socio-economic issues. Worldwide, lives of millions have been benefited by use of ICT tools. India is suppose to be an IT super-power and a major recruiting ground for ICT professionals. Being the force behind many of the ICT projects implemented even in rural areas of developed countries, these professional have been instrumental in bringing around considerable change in rural lives globally. Strangely the same could not be achieved in India due to the absence of basic telecommunication infrastructure. India has a large number of rural villages that do not have telephone connectivity. Over the period of time, this has resulted in a glaring digital divide between rural and urban India. Bridging this digital gap requires considerable investments.

Telecommunication, along with electricity and transport, has been identified as key infrastructure sector for building tomorrows India. The sector, better known globally as Information and Communication Technologies (ICT), is one of the prime support services needed as stimulus for rapid growth and modernization of various sectors of the economy and is also vital for social development of the country. Surveys have shown that every single effect in the telecom sector has many fold effect in the economy of a country. Another key area to attain the goal of accelerated economic development and social change is the provision of telecom services in rural areas. The aggressive expansion of Telecom infrastructure in geographically remote parts of the country is very much essential for unleashing the latent economic energies and market forces in these regions.

INTRODUCTION

India, the second largest populated country of the world, is predominantly rural in nature. Of the 1.027 billion Indians, 741 million live in 638635 villages scattered all across the country. The population density in rural India is around 300 per sq km , which is quiet high in comparison with most of the other countries. Despite this the socio-economic conditions of most of the villages has been pathetic. The literacy rate in rural parts of India is 49.4% as compared to 70% in urban India. The lopsided development is further suggested by the fact that three out of every four villages do not even have the primary health centre. Over 70 % of the rural population contributes to only 24% of GDP. Poor infrastructure and lack of banking facility have further hampered the economic growth in rural areas. Information and Communication Technologies (ICT) have been seen as a major tool that can address many of these socio-economic issues. Worldwide, lives of millions have been benefited by use of ICT tools. India is suppose to be an IT super-power and a major recruiting ground for ICT professionals. Being the force behind many of the ICT projects implemented even in rural areas of developed countries, these professional have been instrumental in bringing around considerable change in rural lives globally. Strangely the same could not be achieved in India due to the absence of basic telecommunication infrastructure. India has a large number of rural villages that do not have telephone connectivity. Over the period of time, this has resulted in a glaring digital divide between rural and urban India. Bridging this digital gap requires considerable investments.

Telecommunication, along with electricity and transport, has been identified as key infrastructure sector for building tomorrows India. The sector, better known globally as Information and Communication Technologies (ICT), is one of the prime support services needed as stimulus for rapid growth and modernization of various sectors of the economy and is also vital for social development of the country. Surveys have shown that every single effect in the telecom sector has many fold effect in the economy of a country. Another key area to attain the goal of accelerated economic development and social change is the provision of telecom services in rural areas. The aggressive expansion of Telecom infrastructure in geographically remote parts of the country is very much essential for unleashing the latent economic energies and market forces in these regions.

Though disparities between the telecom infrastructure of the urban and rural areas are common to all countries, in India this is a continuing source of concern because of declining trend and will become further aggravated unless innovative policies are evolved to accelerate the rural telecom development. For the same it is necessary to understand the underlying dimensions of the low tele-density in rural India.

REASONS FOR POOR TELE-DENSITY IN RURAL INDIA

The rural areas are characterized by sparse population having poor purchasing power. The basic infrastructure viz. electricity and transport is inadequate. In such areas the public interest in telecom facility is caught in a typical cart and horse situation where in absence of telecommunication facility the public interest has not been stimulated. It is not surprising that out of 6,07,491 village is India only about 0.53 million have direct access to telephone facility. With the advent of liberalization in telecom sector all private and government based telecom companies have been concentrating on providing services in big cities and towns to maximize profits. Presently the provision of telecom services in rural areas is typified by high set up cost and low returns. These typical socio-economic conditions, coupled with poor geographical spread has resulted in declining growth of telecommunications infrastructure in rural India. Though investment in telecommunication infrastructure has jumped from 3.6 percent of GDP in seventh plan to 13% of GDP in Ninth Plan, half of the total telephones in India are concentrated in Metropolitan and 100 other capital/commercial cities.

REASONS FOR POOR TELE-DENSITY IN RURAL INDIA

The rural areas are characterized by sparse population having poor purchasing power. The basic infrastructure viz. electricity and transport is inadequate. In such areas the public interest in telecom facility is caught in a typical cart and horse situation where in absence of telecommunication facility the public interest has not been stimulated. It is not surprising that out of 6,07,491 village is India only about 0.53 million have direct access to telephone facility. With the advent of liberalization in telecom sector all private and government based telecom companies have been concentrating on providing services in big cities and towns to maximize profits. Presently the provision of telecom services in rural areas is typified by high set up cost and low returns. These typical socio-economic conditions, coupled with poor geographical spread has resulted in declining growth of telecommunications infrastructure in rural India. Though investment in telecommunication infrastructure has jumped from 3.6 percent of GDP in seventh plan to 13% of GDP in Ninth Plan, half of the total telephones in India are concentrated in Metropolitan and 100 other capital/commercial cities.

The private and now even public telecom operators are not willing to set up of infrastructure in such sparsely populated areas because of the costs involved. To add to injury, the returns are not very sustainable and will remain low in near future till the tele-density improves. The last mile connectivity costs have remained one of the biggest hurdles in providing cheap communication facilities to users. Those who have already built some network in rural areas are not willing to share it with others as they see it as big first move competitive advantage. Poor transportation facilities, irritant power supply, unavailability of spares and technical man-power has resulted in high maintenance costs which further increases losses to operators in such areas.

STEPS TAKEN TILL DATE TO INCREASE RURAL TELE-DENSITY

Before liberalization, universal service objectives have been met by the DOT through a series of programs like Long Distance Public Telephone Program (progressively increasing the scope to the provision of a public telephone within 5 kms of any habitation one telephone in a hexagon of size 5 Square Kilometers), Gram Panchayat Phone (one phone in each Gram Panchayat), and Village Public Telephone Program (one phone in each revenue village) to provide access to voice services. While liberalizing the access segment, post NTP 1994, specific VPT roll out obligations were specified in the licenses.

Post liberalization the various “state interventions” or policy measures taken to increase tele-density in rural India can be grouped under various heads as follows –

1) Tariff Policy - Rural & Urban fixed rentals were traditionally below cost. Mobile tariffs, when specified earlier, were cost based. In 2003, urban fixed tariffs were forborne. However, rural fixed rentals are still regulated and range from Rs. 70 - 280 depending on the exchange capacity. The service provider is allowed to give lower tariffs under alternative tariff package.

2) USO Fund Policy - In 2002, Universal Obligation Service (USO) Fund was established to fund specific USO targets set by NTP 99. The USO levy is presently 5% of AGR and comes out of the license fees paid to the government. However, the implementation of Universal Service Obligation is through a multi-layered bidding process. The Fund is being administered by the Department of Telecom through Universal Service Fund Administrator. On 9th January 2004, the Indian Telegraph Act 1885 was amended to provide the USO Fund a statutory non-lapsable status. The Act states -

“Universal Service Obligation” means the obligation to provide access to basic telegraph services to people in rural and remote areas at affordable and reasonable prices”. The USO aims to fund voice access in remaining villages, low speed data in 35000 villages, high speed data access in about 5400 villages, subsidy for DELs in rural and/or remote SDCAs (486 out of 2648) . At present about 5% of adjusted gross revenue is collected which is estimated at about Rs 3000 Crores for 2004-05. But the disbursement of fund has been an issue. The USO administration has been slow in disbursement of fund and is virtually sitting on more than Rs 30 billions. This has resulted in cautious approach by telecom operators in rolling out their rural obligations.

Liberalization/Competition - Intense competition in mobile services is forcing operators to bring down tariffs and expand coverage to hitherto untouched rural areas. Presently the tariffs for mobile telephony in India have all the more turned one of the lowest in the world. Some reports suggest that tariffs in India are about 50% lower than that of its neighbors, Pakistan and Sri Lanka. This is the reason for high mobile growth in that country. The number of telephones in India, the world’s fifth-largest telecom market, has crossed 100 million connections and the customer base is likely to touch 250 million by 2007. The rates seem to be further going south wards. In April 2005 - a one-minute, local calls costs just 3 cents compared with 8 cents earlier. The regulator in India – TRAI has stopped regulating the rates of mobile services in India for almost couple of years and the prices are forborne. Thus we see that competition has really made the Indian mobile market affordable to citizens and have encouraged the operators to set up their network in rural India.

3) Termination charges - Rural termination charges have been kept same as urban termination charge to give boost to rural telephony

4) Access deficit charges (ADC) – This is a charge imposed to cover the deficits in provision of fixed lines in rural and urban areas. Funding to the extent of Rs 53.40 billions per annum has been provided to state PSUs through collection of ADC. Recently ADC has been reduced from 30% of the sectoral revenue to 10% to make services more competitive.

5) Government funding – Government has provided license fees reimbursement to BSNL (Rs 23 Billions) in lieu of commitment to provide 10 lakh rural DELs. Encouraged by such supports the state owned incumbent operator is planning to invest Rs 84 Billions for expansion of its network in rural areas.

6) Roll-out obligations – Government of India has fixed certain roll-out obligations to all operators to ensure that their services are mandatorilly started in rural areas. For e.g. access providers have to cover 50% of District Head Quarters, National Long Distance Operators have to setup Point Of Presences in every Long Distance Charging Areas (LDCA). The revised roll out obligation for National Long Distance (NLD) services are also under consideration.

Though, some advancement has been made towards improving the rural connectivity, the gains are marginal. A lot needs to be done and that too at much greater pace. If information and Communication Technology has to play a major role in improvement of the life of India’s rural population, the telecom infrastructure backbone has to be considerably strengthened in these areas.

DIGITAL DIVIDE – THE INTERNATIONAL PERSPECTIVE

The problem of digital divide is not unique to India but exists in almost all countries of the world in one form or other. Having looked at the severity of the problem in India, the reasons for its existence and the efforts done till date for bridging the digital divide, it becomes logical to scan the world horizon and look for policy initiatives taken in emerging economies for addressing the problem and implement them in India after customizing them to suit the local needs.

The ICT development indices report released by United Nations Conference on Trade and Development (UNCTAD) shows that during 1995-2002 countries like Egypt, Mexico, China & South Korea have shown remarkable progress in increasing the penetration of ICT amongst masses. Scanning the world horizon, we find that rapid growth in telecommunications have been either demand driven like in China or state-pushed like in South Korea and Egypt. The growth of ICT in urban India has been mainly demand driven. To increase the penetration of ICT in rural India will require greater policy leadership and initiative from state. Overall ICT usage and penetration in the country has still lagged behind international averages. At today’s levels, though, Indians are expected to pay 60 times more than subscribers in Korea for the same throughput, which translates to 1,200 times more when considering affordability measures based on GDP per capita comparison. As recently as 1996, Korea had internet subscriber penetration under 2%, and broadband reached close to 1% penetration only in 1999. In the five years since, however, broadband has become a way of life for Koreans, and it permeates in everything they do. Today, almost 80% of households have broadband connections, and in 2002, US$148 billion, nearly 30% of their GDP, was transacted on the internet. China has also launched a major broadband expansion program. The success in other countries in making telecom services as the basic platform on which economic and commercial growth is achieved, can also be replicated in India, particularly for rural areas.

Though, some advancement has been made towards improving the rural connectivity, the gains are marginal. A lot needs to be done and that too at much greater pace. If information and Communication Technology has to play a major role in improvement of the life of India’s rural population, the telecom infrastructure backbone has to be considerably strengthened in these areas.

DIGITAL DIVIDE – THE INTERNATIONAL PERSPECTIVE

The problem of digital divide is not unique to India but exists in almost all countries of the world in one form or other. Having looked at the severity of the problem in India, the reasons for its existence and the efforts done till date for bridging the digital divide, it becomes logical to scan the world horizon and look for policy initiatives taken in emerging economies for addressing the problem and implement them in India after customizing them to suit the local needs.

The ICT development indices report released by United Nations Conference on Trade and Development (UNCTAD) shows that during 1995-2002 countries like Egypt, Mexico, China & South Korea have shown remarkable progress in increasing the penetration of ICT amongst masses. Scanning the world horizon, we find that rapid growth in telecommunications have been either demand driven like in China or state-pushed like in South Korea and Egypt. The growth of ICT in urban India has been mainly demand driven. To increase the penetration of ICT in rural India will require greater policy leadership and initiative from state. Overall ICT usage and penetration in the country has still lagged behind international averages. At today’s levels, though, Indians are expected to pay 60 times more than subscribers in Korea for the same throughput, which translates to 1,200 times more when considering affordability measures based on GDP per capita comparison. As recently as 1996, Korea had internet subscriber penetration under 2%, and broadband reached close to 1% penetration only in 1999. In the five years since, however, broadband has become a way of life for Koreans, and it permeates in everything they do. Today, almost 80% of households have broadband connections, and in 2002, US$148 billion, nearly 30% of their GDP, was transacted on the internet. China has also launched a major broadband expansion program. The success in other countries in making telecom services as the basic platform on which economic and commercial growth is achieved, can also be replicated in India, particularly for rural areas.

Egypt also has a strong tradition of central government and reliance on government to provide services and policy leadership. During 1995 to 2002, Egypt rose strongly in ICT diffusion ranking from 154th position to 112th position worldwide despite the fact that its economy has suffered a slowdown and deterioration in economic conditions since 2000, which has led to reductions in real wages and consumer purchasing power. Egypt has encouraged investment in infrastructure and has been building public-private collaboration in ICT deployment. Its experiment with models of shared public access in the IT Clubs can be replicated in developing countries like India where the PC penetration is still dismal.

BRIDGING THE DIVIDE – LESSONS FROM EGYPT

Arab Republic of Egypt, the most populated Arab state, has 55% of its population living in rural areas (as per latest census estimates of 1999) . With GDP growth rate averaging above 5, Egypt is ranked at 119th as compared to 127th of India in United Nations Development Program’s (UNDP) Human Development Index(HDI) . After formation of Ministry of Communication and Information Technology (MCIT) in 1999, Egypt has raced ahead on its path of Information society initiative. The Telecom and Information Technology policy of Egypt has tried to bridge the digital divide within the country and its initiatives to empower the citizens with information has evolved around three basic policy pillars

BRIDGING THE DIVIDE – LESSONS FROM EGYPT

Arab Republic of Egypt, the most populated Arab state, has 55% of its population living in rural areas (as per latest census estimates of 1999) . With GDP growth rate averaging above 5, Egypt is ranked at 119th as compared to 127th of India in United Nations Development Program’s (UNDP) Human Development Index(HDI) . After formation of Ministry of Communication and Information Technology (MCIT) in 1999, Egypt has raced ahead on its path of Information society initiative. The Telecom and Information Technology policy of Egypt has tried to bridge the digital divide within the country and its initiatives to empower the citizens with information has evolved around three basic policy pillars

1. Heavy emphasis on research and development in traditional and new industries to allow Egypt to become and remain a world class competitor. Research and development centres of excellence have been established to bring together professionals, private sector initiatives and educational establishments.

2. To allow Egypt to become an attractive foreign investment hub, favorable regulatory policies have been put in place. The foreign investment inflow has not only been source of employment generation but is also benefiting Egypt through technology spin – offs. Setting up of National Telecom Regulatory Authority (NTRA) and Initial Public Offering (IPO) of Telecom Egypt are part of such initiatives for freer market.

3. The third and most crucial policy initiative has been of providing total access of the Internet and related services to encourage entrepreneurs and markets to fulfill their potential. This policy of e-Access has concentrated on ICT capacity building in the community by reaching out to the poorer and rural areas.

The third pillar of Egypt’s ICT policy has been implemented through several micro level programs which are based on three key success factors for ICT diffusion amongst masses i.e. awareness, accessibility and affordability.

These micro-level e-Access programs are uniquely developed to suit the Egyptian conditions and are of special interest to emerging economies like India. These programs have helped in bridging the digital divide within Egypt’s industries, people, and wide ranging cultures and have helped the country “to move forward as a whole, and not just in certain sectors.” These micro-level policies or programs combine the imaginative use of emerging technologies with creative Public Private Partnerships and Multi Stakeholder Partnerships to accelerate development. The e-Access policies have been built over the growth of telecom infrastructure and guarantee universal, easy, affordable and rapid access for all citizens to ICT. They have become instrumental in stimulating awareness of the potential uses and benefits of ICT to masses and classes alike. The initiative not only focuses on hardware and software but also emphasizes the development of flexible and innovative tools and channels. Of the various micro-level policy initiatives the two which can be considered to be of interest for implementation in India are -

The third pillar of Egypt’s ICT policy has been implemented through several micro level programs which are based on three key success factors for ICT diffusion amongst masses i.e. awareness, accessibility and affordability.

These micro-level e-Access programs are uniquely developed to suit the Egyptian conditions and are of special interest to emerging economies like India. These programs have helped in bridging the digital divide within Egypt’s industries, people, and wide ranging cultures and have helped the country “to move forward as a whole, and not just in certain sectors.” These micro-level policies or programs combine the imaginative use of emerging technologies with creative Public Private Partnerships and Multi Stakeholder Partnerships to accelerate development. The e-Access policies have been built over the growth of telecom infrastructure and guarantee universal, easy, affordable and rapid access for all citizens to ICT. They have become instrumental in stimulating awareness of the potential uses and benefits of ICT to masses and classes alike. The initiative not only focuses on hardware and software but also emphasizes the development of flexible and innovative tools and channels. Of the various micro-level policy initiatives the two which can be considered to be of interest for implementation in India are -

1. PC for Community Policy – The PC for community policy evolved out of PC for every home program that was launched by MCIT in Egypt in November 2002 and aimed at providing hardware so as to achieve a penetration of one PC per three families. The policy covered provision of laptops to individuals in the business sector. The policy is built around the concepts of availability and affordability. The aim of the PC for Community initiative is to provide end users with computers at prices affordable for the average user, mainly by offering simple and approved credit schemes. A parallel scheme was also conceived as Notebook for Every Professional to provide an opportunity for business professionals to adapt to changes in working culture. The policy aimed at distributing six million computers over seven year period in partnership with private sector to develop the required hardware. The policy has two broad objectives –

A) To boost the hardware manufacturing sector and to provide easy and

B) Affordable finance option for citizens for purchase of the PCs.

The first objective is achieved through creation of design centre for computer development and cooperating with international computer companies for manufacturing PC components.

A) To boost the hardware manufacturing sector and to provide easy and

B) Affordable finance option for citizens for purchase of the PCs.

The first objective is achieved through creation of design centre for computer development and cooperating with international computer companies for manufacturing PC components.

While the second objective is achieved through tie up with Banque Misr for providing LE 630 million and with the National Bank of Egypt for providing LE one billion to finance the initiative. The Egypt Telecom is one of the partners in project whose responsibility is to provide the private telephone line as collateral to finance the purchase of PC. It also provides its outlets for registration and collects the monthly installments through phone line bills. Credit risk Insurance company has to cover the risk of non-payment. The guarantee of phone line has proved the critical factor in success of the scheme as it helps in identification of genuineness of loan seeker and also helps periodic collection of installments through telephone bills. For the same, the Banque Misr and NBE branches have been provided with systems remotely connected to Egypt Telecom’s database to assist them. MCIT’s role is to certify and monitor the performance of the companies from the private sector that have joined this program. The Ministry has worked this year to simplify procedures even further for securing loans and for purchasing the equipment. Citizens receive a loan by providing the guarantee of a phone line and a personal ID. The payment period has been extended to 40 months, and there are now an expanded number of locations to apply for loans guaranteed by a phone line. By the end of 2004, this system was available throughout the country in 350 branches of the National Bank of Egypt and 450 branches of Banque Misr.

The PC for community policy offers affordable, Internet-enabled family computers payable through installments, with no collateral and no deposit required, and the only guarantee that is needed is a fixed telephone line. The target is to reach 100,000 PCs sold annually to lower market segments and to open the market to Egyptian and foreign investors. Twenty two Egyptian private companies are involved in the manufacture of these locally-assembled PCs, along with four international notebook computer manufacturers as well as a number of major international producers of hardware components.

In 2004 a hotline at the Xceed Contact Centre was set up to provide customer service, answer inquiries, and manage complaints, for new participants in the scheme. This targeted the awareness building part of the policy. In addition to this customer confidence in the schemes has been boosted by establishing extended warranties on products supplied from twelve to thirty six months. At present there are over 500 distributors, sales outlets, and service and maintenance centers that are involved in the scheme.

In 2004 a hotline at the Xceed Contact Centre was set up to provide customer service, answer inquiries, and manage complaints, for new participants in the scheme. This targeted the awareness building part of the policy. In addition to this customer confidence in the schemes has been boosted by establishing extended warranties on products supplied from twelve to thirty six months. At present there are over 500 distributors, sales outlets, and service and maintenance centers that are involved in the scheme.

The advantages of this policy initiative can be summarized as follows –

i) Strengthen domestic capabilities in hardware manufacturing.

ii) Attract foreign investment in areas of high technology and software engineering

iii) Boost economic activity and development – the sale of PCs has grown at 25% per annum

iv) The PC manufacturers have started looking for export opportunities in Arab region

v) Employment generation through distributors, sales outlet and service and centers

vi) Requirement of locally developed software application has given boost to domestic software industry

The figure of PCs supplied by September 2005 was 118,616 and 287 notebooks. Encouraged by the success of the program Egypt government is looking forward to launch future schemes as PC for Every student and Teacher. By 2007, 14 million users are expected to benefit from 4 million PCs.

2. IT Club Policy – The IT club policy was started by MCIT to provide access to technology in under-privileged areas so that all Egyptian citizens have the opportunity to learn new skills and expand their horizons. The model was developed to offer a communal solution to one of the biggest problem encountered by emerging economy to develop Information society i.e. the problem of affordability, accessibility and awareness. The IT Clubs model is another Public Private Partnership to bring affordable Internet access throughout the country to those who cannot afford to own a PC. For nominal fees reaching LE 1 (about US$ 0.20) per hour and by providing hardware, software, and Internet connections, the government has made IT a daily reality for many who previously had little experience with the new technologies. In each club an instructor is available to train new users in basic keyboard skills, software applications and web design. The university graduates can join the “Training of trainers” program to become ITC knowledge trainers who will provide courses at the IT clubs. This train the trainers program has increased the opportunity of employment to university graduates. To reinforce the concept of community at each club, the managers must live in the same governate, providing the added benefit of being familiar with the needs and interests of local community.

The MCIT is responsible for providing all the necessary equipment – computers, printers, peripherals, Internet access, LAN and Server. A site license has been arranged with Microsoft for windows operating system and Microsoft office word. The private sector partners provide the space, infrastructure, utilities, furniture and security for the club. MCIT has established IT Clubs in youth centers, cultural centers, non-governmental organizations, universities, schools, syndicates, public libraries, local authorities and information centers in all governorates. The club is generally built over 50 sq mater space and is equipped with restrooms, air-conditioning etc. MCIT is forming partnerships with Egyptian and international entrepreneurs to accelerate the rate of expansion of these clubs throughout the country. In 2004, the project collaborated with the UNDP and Unlimited Potential of Microsoft and the Korean Agency for Digital Opportunity and Promotion to achieve its objectives. More than 20 ISPs have already offered to jumpstart the IT Clubs. Citizens who join the IT Clubs can improve their skills with computer applications and through extended services like electronic library. Clubs are now also training participants for the Egyptian Olympiad in Informatics and have dedicated space at clubs for people with special needs. IT clubs are providing access to e-government services, providing e-learning services, and developing a Mega-Club portal with bilingual content - www.ict-megaclub.com.eg . Under the existing government sponsored program, the IT club begins operation with virtually zero debt, so revenues generated are invested in sustaining and improving the club.

IT Club is one of the best policy initiatives to tackle the problems that come with the information age i.e. to make available the benefits of digitally connected world to the citizens at affordable price. The problem with developing world is the paying capacity of the individuals both for procuring the hardware and for paying recurring charges for internet access. The policy of setting up of IT Clubs takes care of these issues. By providing shared access to the community the citizens need not purchase the computers. Further since the returns from business are not adequate in rural and remote areas, the chances of setting up of cyber cafes by private sector are remote. By setting up the IT clubs the Egypt government has ensured that the required awareness is created amongst the masses. Further the IT clubs have developed into major training centers for the basic training in IT. The long term goal of setting such clubs is to develop interest and skills of community in IT so that the business case of setting such cyber clubs by private entrepreneurs becomes viable in near future.

The It Club policy also serves the objective of Human Resource development by training citizens in all age groups to develop their skills and improve productivity. The IT clubs are located in easily accessible places/organizations like schools, libraries, youth centers etc. which are already in business of educating and empowering youths. The location of IT clubs is chosen carefully to ensure setting up of these clubs in low income areas that previously did not have affordable access to the internet or modern technology. The condition that the trainers or managers must have received a university degree and should be currently unemployed has helped in generation of jobs. The selection of trainer is based on aptitude test and this ensures that good quality trainers are inducted for the job. The pivotal factor for success of such policy initiatives is the cost that has to be born by the users for internet access. The charges have been kept extremely low at LE 1 per hours which are much less than what private cyber cafes will be offering in Cairo. The initiative has helped in diffusion of use of ICT in small business people who with the help of trainers in IT clubs has started using spreadsheets, presentations and websites. The spectrum of training courses offered at these clubs range from basic keyboarding to designing websites and launching e-businesses. Individual members can even request for courses that suite their demands. The club charges are based on either monthly subscription fees which are in packages of 10-20 hours or on hourly rate access. Club membership hours can be used to participate in any of the activities of club like surfing the internet, taking training courses or utilizing the software libraries.

The IT Club policy has resulted in increased demand for use of internet and hence the clubs are being set up with leased line connectivity. The benefits of the IT Club policy include raising of the IT awareness, increasing computer literacy, boost societal integration, generate employment, maximize use of resources at local level and boost the economy through increased skills and productivity. MCIT projects to grow the number of IT club from 1000 to 2800 by June 2007. The average number of users is currently 1000 per club. This way 2.8 million projected users can be ensured through this policy initiative.

SUGGESTIONS FOR IMPLEMENTATION OF THESE POLICIES IN INDIA

The emphasis of Indian policy makers for bridging the digital divide has been mainly on improving tele-density. Little thought has been given to the fact the providing connectivity does not ensure the usage of the same by the citizens to access information. In today’s world, which is shrinking day by day – digitally - the empowerment of the masses through use of internet is crucial. This does not mean that emphasis should not be given to improve tele-density.

SUGGESTIONS FOR IMPLEMENTATION OF THESE POLICIES IN INDIA

The emphasis of Indian policy makers for bridging the digital divide has been mainly on improving tele-density. Little thought has been given to the fact the providing connectivity does not ensure the usage of the same by the citizens to access information. In today’s world, which is shrinking day by day – digitally - the empowerment of the masses through use of internet is crucial. This does not mean that emphasis should not be given to improve tele-density.

In fact the priority should be two pronged –

A) To provide telecom infrastructure in hitherto unconnected rural areas and

B) Concentrate on extending data services like internet in rural areas which have already experienced the benefits of connectivity. For the same it is suggested that the efforts should first be concentrated to set up community tele-centers (on the model of IT Clubs of Egypt) in all villages having more than 5000 population. This way by setting up some 20,000 IT clubs, more than 25% of rural population can have shared access to internet (Refer to following table). The policy of PC for community should be implemented throughout India with some extra benefits to those living in rural areas.

POPULATION DISTRIBUTION IN INDIAN VILLAGES

Population No of Villages % of total villages

POPULATION DISTRIBUTION IN INDIAN VILLAGES

Population No of Villages % of total villages

200-500 127054 21.4

501-1000 144,817 24.4

1001-2000 129,662 21.9

2001-5000 80,313 13.5

5001-10000 18,758 3.2

The biggest hindrance that can come in implementation of both these policies is the requirement of funds. As already explained, the same can be provided through Universal Service Obligation (USO) fund. A lot of unutilized fund is lying with the USO Administrator. Even in coming years the collection of USO levy is going to exceed its disbursement as pointed out by recommendation of Telecom Regulatory Authority of India (TRAI) to Government of India. The following table shows the amount of excess funds that will be available with Government of India and these funds can be used for implementation of both the suggested policy initiatives. (Figure are in crores of RS)

Financial Year Collection Disbursement Balance

2002-03 1653.61 300 1353.61

2003-04 2143.22 200 3296.83

2004-05 3457.73 1314.58 2143.15

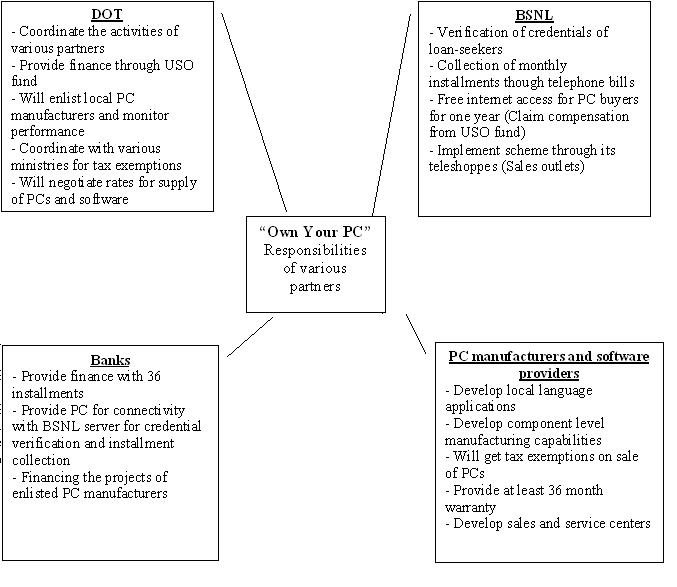

Having seen two major issues of financing and areas of implementation of the two policies the other details on implementations are as follows – 1) Policy of “Own your PC” (On the model of Egyptian policy of “PC for community”) – The policy can be implemented in partnership of the incumbent telecom operator i.e. Bharat Sanchar Nigam Limited(BSNL), Department of Telecommunications, Public sector Insurance companies (Like United India Insurance, Oriental Insurance etc.), Nationalized banks (Like State bank of India, PNB etc), Multinational software provider companies (Like Microsoft, Linux etc.) and Private sector PC manufacturers. The role and duties of each partner in the initiatives are summarized in following figure -

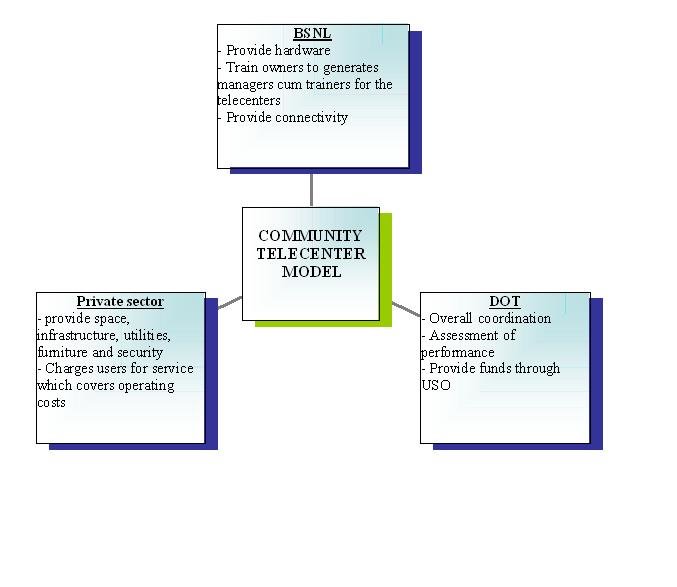

2) Policy of “Community Tele-centers” (Based on the model of IT Club policy of Egypt) - Setting of Community Telecenters will require funds for provision of Server, printer, network(LAN) and PCs( three apart from server which itself can act as a terminal) and peripherals. Considering Cost of PC to be nearly Rs 25,000/- and that of entry level server to be Rs 75,000/- The total cost of setting up the hardware in community tele- centers will be around Rs 200,000/- (per center). Considering the suggestion of setting up these centers in villages having population over 5,000 means that around 20,000 centers are to be established in first phase. This translates into a total cost of Rs 4 billion (Appx 90 million USD). The suggested model with duties and responsibility of various partners are shown in following figure -

Suggested model for the Community telecenters

CONCLUSION

Information & communication technology sector is in a very dynamic stage today. In such a scenario, reform in policies is a continuous process necessitated by dynamics of change & technology innovations. To fill up the huge digital divide present in India immediate policy changes are required so as to make the sector truly liberal. The fact that poor infrastructure along with emblematic socio-economic conditions has resulted in virtual market failure in rural India. The intervention of state though suitable policy measures is the immediate need of the hour. Until and unless 72% of population living in rural India is provided greater access to information, it will be difficult to have appreciable impact on projected social and economic growth. Special rural telecom strategies are to be framed at the National level and state level to bridge this growing digital divide. Even with tremendous growth in the information technology sector, For this development to occur, appropriate regulatory environment and policies need to be established so that the discrepancy in pricing, penetration and type and quality of ICT services within India can be eliminated. Once this happens, only then will there be successful growth and business models in video, broadband, internet and telephony services.

The most stimulating change in telecom today is that apart from PSUs, the private operators are waking up to their rural responsibilities. The saturated urban market is also forcing the players to move towards the untapped rural hinterland. Research shows that socio-economic interests of villages are confined to near by villages or big towns. As the telephone services are made available in all villages the telecom traffic will increase automatically. As the penetrating level goes on increasing, more and more player will automatically step into the rural telecom sector to make it self-sustainable.

A delicate blend of appropriate technological choice in combination with management and financing mechanism supported by Government policies can help penetration of communication services in Rural India. The lessons from the emerging economies like Egypt can easily be customized and implemented in India. The sharing of resources as done in IT Clubs is crucial for countries like India at this stage of development. It should be clearly understood that once the rural telecommunication amplifies, overall social and economic development of country will automatically permeate. Then and only then, India can consolidate its positions as a leading hub of communication systems and IT enabled services and can establish itself as a leader in new disciplines such as bioinformatics and biotechnology. Only then, the current change in Information and Communication Technology can become a saga of vanishing myths. Only then, ongoing IT process in India can transform into a “True Revolution”.

Information & communication technology sector is in a very dynamic stage today. In such a scenario, reform in policies is a continuous process necessitated by dynamics of change & technology innovations. To fill up the huge digital divide present in India immediate policy changes are required so as to make the sector truly liberal. The fact that poor infrastructure along with emblematic socio-economic conditions has resulted in virtual market failure in rural India. The intervention of state though suitable policy measures is the immediate need of the hour. Until and unless 72% of population living in rural India is provided greater access to information, it will be difficult to have appreciable impact on projected social and economic growth. Special rural telecom strategies are to be framed at the National level and state level to bridge this growing digital divide. Even with tremendous growth in the information technology sector, For this development to occur, appropriate regulatory environment and policies need to be established so that the discrepancy in pricing, penetration and type and quality of ICT services within India can be eliminated. Once this happens, only then will there be successful growth and business models in video, broadband, internet and telephony services.

The most stimulating change in telecom today is that apart from PSUs, the private operators are waking up to their rural responsibilities. The saturated urban market is also forcing the players to move towards the untapped rural hinterland. Research shows that socio-economic interests of villages are confined to near by villages or big towns. As the telephone services are made available in all villages the telecom traffic will increase automatically. As the penetrating level goes on increasing, more and more player will automatically step into the rural telecom sector to make it self-sustainable.

A delicate blend of appropriate technological choice in combination with management and financing mechanism supported by Government policies can help penetration of communication services in Rural India. The lessons from the emerging economies like Egypt can easily be customized and implemented in India. The sharing of resources as done in IT Clubs is crucial for countries like India at this stage of development. It should be clearly understood that once the rural telecommunication amplifies, overall social and economic development of country will automatically permeate. Then and only then, India can consolidate its positions as a leading hub of communication systems and IT enabled services and can establish itself as a leader in new disciplines such as bioinformatics and biotechnology. Only then, the current change in Information and Communication Technology can become a saga of vanishing myths. Only then, ongoing IT process in India can transform into a “True Revolution”.